Five key takeaways from earnings season

- 05.10.24

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Mega-Cap Tech Continues To Drive S&P 500’s Earnings

- Shareholder-Friendly Activity Is Back!

- Consumers Are Becoming More Discerning

Happy National Small Business Day! Every year on May 10, small businesses are officially recognized for their contributions to the US economy. And rightfully so. Small businesses are the backbone of the US economy. Today, there are over 33 million small businesses operating across the US. Small businesses employ over 61 million employees—nearly half of the entire American workforce. And a record-breaking 5.5 million new business applications were filed in 2023. Truly impressive! Just as small businesses are a key barometer for the nation’s economic health, large public companies drive the trends in earnings. That is why we pay so much attention to earnings season. With 1Q24 earnings season largely compete with over 88% of the S&P 500’s market cap having already reported, here are our five biggest takeaways:

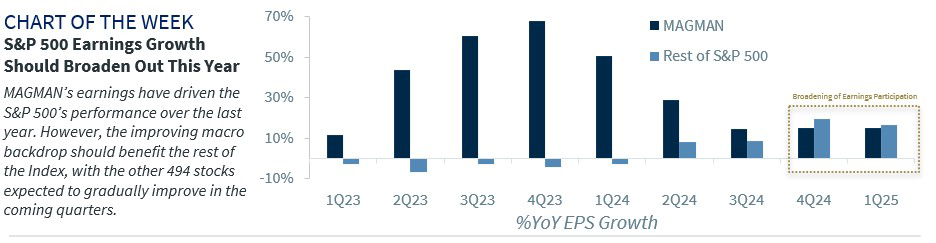

- Mega-Cap Tech Continues To Drive Earnings | Despite elevated valuations, mega-cap tech earnings remain a bright spot, driving the bulk of the S&P 500’s earnings. In fact, the composite of MAGMAN’s earnings (i.e., Microsoft, Apple, Google, Meta, Amazon, and NVIDIA) we track is on pace to climb over 50% YoY. Compare that to the other 494 stocks in the S&P 500, which have roughly flat earnings growth YoY. More important, this is the fifth consecutive quarter that MAGMAN’s earnings have outpaced the rest of the Index. In addition, MAGMAN has had greater top-line sales growth (over 5x higher), stronger net margins (~2.5x greater) and bigger earnings beats (~12% versus 8%) than the rest of the Index. Our composite of mega-cap tech (i.e., MAGMAN) has strongly outperformed the overall market, (50.9% versus 25.4% over the last 12 months), with their outperformance supported by strong fundamentals and superior earnings results.

- Business Capex Spending Is On The Rise | Early gains in the bull market in late 2022 and 2023 were driven by businesses being rewarded for pivoting to contain costs (i.e., tech layoffs, restructurings) amid an uncertain economic environment. Nearly 1.5 years later, businesses are pivoting again—shifting from cost containment to investing in growth areas (like AI and cloud computing) to support their businesses. This is contributing to CEOs becoming more optimistic about the state of the economy. In fact, the Conference Board’s CEO Confidence survey moved back into expansionary territory (a level above 50) in Q1 for the first time in two years! Some of the biggest beneficiaries of the increased capex spend are tech-related, Communication Services and select areas of Consumer Discretionary stocks. Let’s not forget Industrials (one of our favored sectors), which continue to reap the benefits from all the fiscal spending via the CHIPS, IRA and IIJA legislation in recent years.

- Buybacks Are Back! | With many S&P 500 companies still flush with cash on their balance sheet—to the tune of $2 trillion—management teams are re-focusing on delivering shareholder value. This is evident in dividend growth, which is running at an 8% YoY pace in 2024—above last year’s 5+% pace and the 10-year average of 6.6%. In addition, companies thus far have announced over $180B in stock buybacks in 1Q—yet another sign of improved confidence. In fact, stock buybacks have remained above their 10-year average for 13 consecutive quarters. A continuation of this trend should serve as another tailwind for stocks. Case in point: Meta and Alphabet authorized their first-ever dividend this quarter, and additional repurchases of stock. Apple announced a $110 billion dollar buyback—its biggest in the company’s (and market’s) history! We think this trend will continue.

- Consumers Are Becoming More Discerning | Despite ongoing concerns of consumer fatigue, a big takeaway this earnings season is that consumers, in aggregate, remain healthy and resilient. This was highlighted by some bank and credit card companies, which reported that loan loss reserves (the amount set aside to cover uncollectible debts) remain stable and even decelerated last quarter and delinquency rates remain well below historical averages. Yes, there are signs that consumers are starting to prioritize their spending (i.e., travel remains favored over goods-related areas) and lower-income consumers are feeling the pinch from higher prices (e.g., restaurant, beverage companies), but this is forcing companies to compete on delivering value to capture the discretionary spend. Those who execute well are being rewarded.

- Earnings Growth Is On A Solid Uptrend | Earnings growth has remained positive for three consecutive quarters, with 1Q24 on pace for a 6+% YoY gain. The healthy macro backdrop and optimistic comments about the resilient consumer and business spending suggests forward looking earnings should remain on an uptrend in the coming quarters. In fact, consensus estimates reflect double digit EPS gains in two of the next three quarters, with 2025 earnings estimates around ~$275/share—a 13+% gain YoY. More important, earnings growth is expected to broaden, with the other 494 stocks in the S&P 500 catching up and even outpacing MAGMAN’s earnings later this year. These solid earnings trends, plus optimistic management commentary, leave us confident in our $240 year-end S&P 500 EPS target.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.